Yellow Card’s perspective on regulation in Africa’s largest crypto market

The exchange service, which has operations in over a dozen African markets, weighs in on the state of cryptocurrency regulation in Nigeria

Roughly three years ago, the Central Bank of Nigeria (CBN) embargoed cryptocurrencies from the country’s banking halls. Citing threats to the safety of the system, the Bank with an iron fist barred commercial financial institutions from facilitating digital asset-based transactions.

But, in December 2023, under new leadership, the CBN started walking back the no-bank policy, making allusions to current global trends to see financial authorities willing to regulate virtual asset providers.

Under some conditions, banks can now operate accounts for crypto exchanges. The U-turn raises hope for a market that has been in dire straits since early 2021 when crypto transactions were outlawed overnight.

Several ventures operating in the market resorted to downsizing or pivoting during the wait time, including notables like Quidax, Localbitcoins, Paxful, Lazerpay, and Nestcoin.

One of the companies heralding the tide change in the industry is Yellow Card, a Greater Atlanta-headquartered online platform for buying and selling cryptocurrencies.

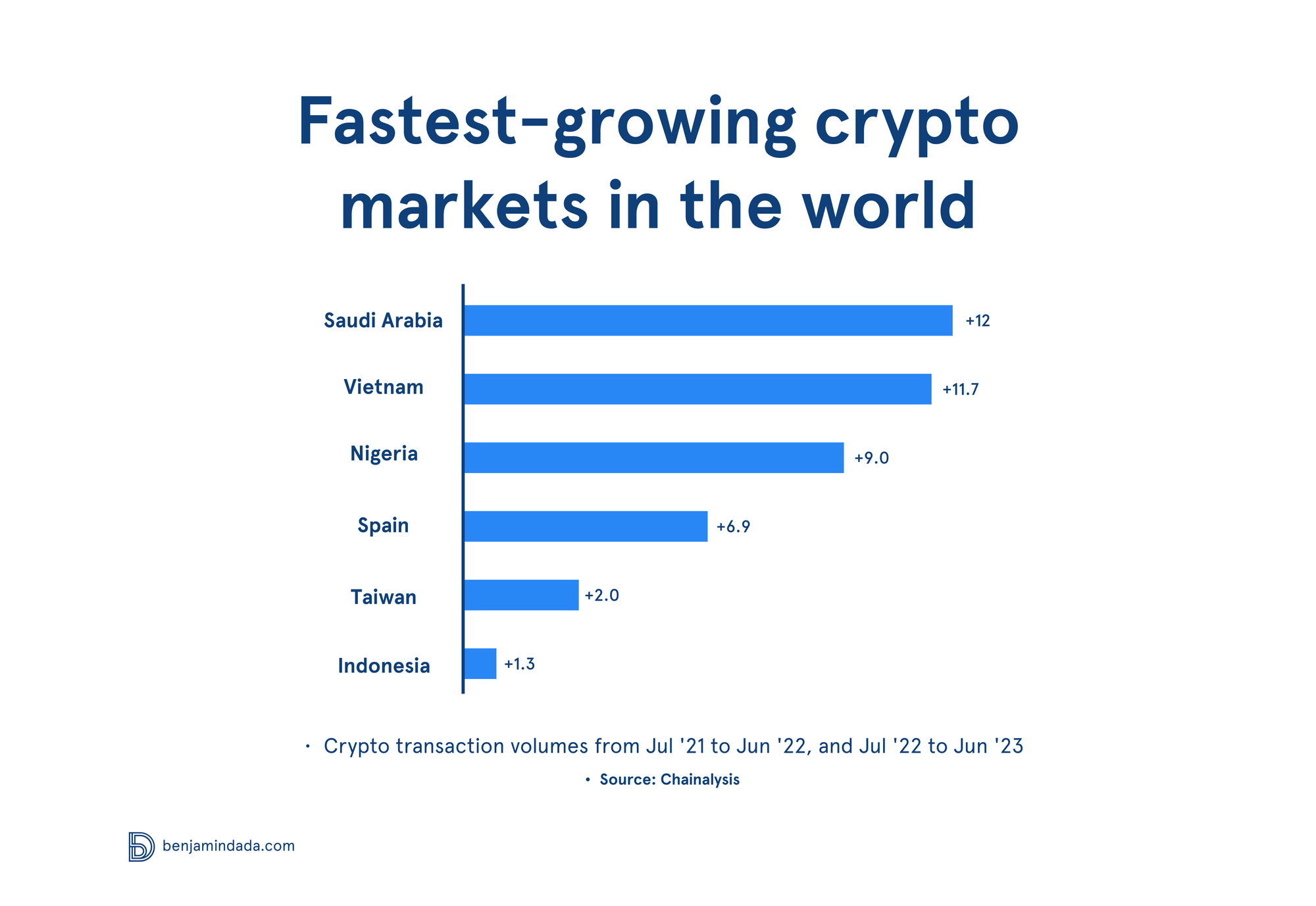

The company operates in up to 20 African markets, including South Africa, Ghana, Kenya, Rwanda, Senegal and Ivory Coast. In 2022, the venture raised $40 million in Series B to drive crypto adoption in the continent.

Hot on the heels of the CBN’s update, the company announced it is seeking a license in Nigeria, as it looks to become one of the first to win regulatory approval.

In this exclusive with Bendada.com, Lasberry Chioma Oludimu, Chief Data Protection Officer and Vice President of Legal, Commercial, and Product at Yellow Card, shares a bird’s-eye view on the state of regulation in Africa’s largest crypto market.

Players have been eagerly monitoring the space for a few years. What have you noticed so far?

Lasberry: We have been keeping an eye on the regulatory side of the space since 2020. We registered in 2018 and started business in 2019.

However, our hopes did not go up until the Securities and Exchange Commission (SEC) published its first statement on digital asset classification and treatment. That gave us a green light that the regulators, including the central bank, would eventually cryptocurrency-based transactions.

What we did not know was how long it would take to completely set up the needed framework and implement it. The intentions were obvious but there was no definite timeline.

In the SEC’s 2020 circular, cryptocurrencies were classified as digital assets “until proven otherwise”, which means the regulatory framework [now] falls under their purview. From then, we started keeping tabs on the regulatory environment, expecting further information from the SEC.

While the ecosystem was still waiting for more guidelines, the CBN love-lettered banks do not facilitate cryptocurrency transactions.

That was a major setback, one that dashed a lot of hopes. On our part, it made us divert attention from Nigeria to other African markets where we were already operating.

It was a dramatic start. But at a time a change was in the works. Where was the turning point?

Lasberry: Amid the restrictions, in 2022 the SEC published rules on the issuance, offering, and custody of digital assets.

The question was how were the exchanges meant to implement them when they did not have access to commercial bank accounts. There was a need to go beyond peer-to-peer (P2P). Unable to implement the regulations, players operated along an unclear path, even after a series of conversations between stakeholders and the regulators.

Then, in December 2023, the CBN released a statement allowing exchanges to open trading accounts on certain conditions, one of which is licensing.

It is not [actually] a strange string of developments because Nigeria is more open-minded compared to a lot of other African countries where the regulators are unwilling to negotiate. In some of these markets, customers are left to trade with the operators at their own risk.

In Nigeria, we were seeing some kind of guidance, even if delayed. We are hopeful that eventually, the SEC’s rules from 2022 can now be implemented. The end game is to follow up with this to the stage where we know we have the regulators’ full support.

Beyond licensing and access to bank accounts, what does the new regulation mean for the ecosystem?

Lasberry: Actors that shuttered along the line were, mostly affected by regulation, unable to raise funds or acquire active users, and as such were unsure about profitability. There was a lot of uncertainty as to being able to keep up.

This turnout will help build confidence and trust in the sector, particularly for the people who are investing in the exchanges and those who will be using the trading platforms.

Since 2021, many have become skeptical about cryptocurrencies in the country, and by extension, do not trust the sector. Some did not even have a proper interpretation of the central bank’s stance on the matter. It did not outrightly ban crypto but only disallowed banks from using them for transactions.

The clarifications will help players build trust with their investors and customers without worrying about their survival. Once you have a license, you can confidently say anywhere [that] you operate legitimately.

That takes us to longevity; when there is regulation, players can do business for a long time. That way, it is easy to convince both users and investors this is a safe space to play in.

It would bring the ecosystem together in the long run. What else do you think would change?

Lasberry: It will also bring about innovation in the sector. With exchanges trying to survive the storm, there has barely been any in the past few years.

While it is evident from global analyses that Nigeria is one of the biggest crypto markets, it is impossible to compare what is obtainable with what is possible when there is clear regulation.

Now that players have a better framework, can obtain a license, and interact with the regulator when issues arise, they have more time to think about innovating their products.

They can start looking for ways to add value to their offerings in view of becoming household names in the country. That would expand crypto’s use case.

When the SEC starts issuing licenses, FX inflows will improve. That is because we are not just trading crypto here in Nigeria; we also have transactions from people outside the country. The possibility of the regulation contributing to an increase in FX is very high. Players are likely to increase as a result.

New exchanges and more activities mean more employment in the sector. Now that there is a green light of sorts from the authorities, more young people would be recruited into the industry.

In the grander scheme of things, a business can only survive and thrive where there is regulation.

Agreed, it is necessary for business survival. Looking at the standing rules, what can be improved?

Lasberry: No regulation is perfect. That is why you see things like amendment bill debates. Regulators are not the players, so their views might be slightly different from what is obtainable.

As such, there is an opportunity to miss some things in the cause of implementation. That is where the need for amendment processes comes in.

There are some provisions in the recent guidelines that are still unclear. For example, the central bank says banks can open accounts for exchanges that have been licensed.

But, per the SEC’s requirements, exchanges must have proof of up to N500 million in paid-up share capital before applying for a license. How do you get a bank statement without a bank account? Which comes first, having the license or proving there is that amount of money in the bank?

From the SEC’s angle, the capital needs to be imported and shares paid before a license can be obtained. But, from the CBN, a license is needed to approach banks.

Also, players are required to pay some fees to regulators. Since we cannot do so in cash, it has to be with bank transfers. That means we need to move money from company accounts or generate manager's cheques. How do we manage this without access to banks? The good news is the SEC is looking into it.

Before an account can fund or receive funds from crypto platforms, there should be full KYC. But there has not been any clarification on that.

I believe ultimately, both agencies can liaise with each other on ways to make things more seamless and then inform the general public of their conclusion.

Comments ()